One year on: the impact of COVID-19 on artists in Malta.

The opt-in online survey was launched on the 16th of March 2021 and closed on the 7th of April 2021. During this period, new measures came into effect leading to the closure of cinemas, theatre and museums. This meant that any artistic events and arts education activities that were going to be held using the mitigations measures imposed before March 2021 had to be postponed or cancelled. Some key observations for this survey:

- Concerns on a creative brain drain. Respondents who were unemployed in the arts, but engaged in other sectors increased from 2.7% in March 2020 to 14.5% in March 2021.

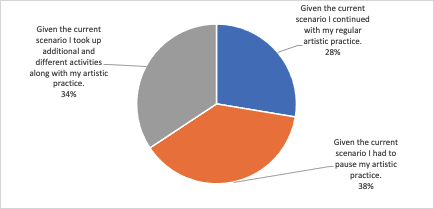

- 38% of the respondents report to have stopped their artistic activity altogether.

- In March 2020 the ratio of activities per respondent was 8. In March 2021 the ratio was of just below 4 activities per respondent. These were once again cancelled or postponed due to the new restrictions.

- The organisation of seminars and conferences and the delivery of arts education have registered high levels of adaptability and are positively correlated with the ability, albeit with limitations, to move the activity online.

- Respondents who earn an income exclusively from the arts continue to suffer severe income losses. The highest bracket (EUR 45K +) in 2019 diminished whilst the brackets EUR 2.5K to EUR 5K and EUR 5K and EUR 10K registered significant increases in 2020.

- Respondents forecast their income to bounce back but recovery is expected to be at a very slow pace and over a long period of time.

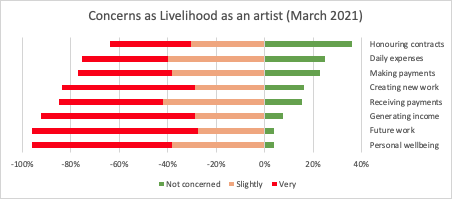

- As indicated in previous surveys, generating income, the prospects of future work and personal wellbeing are of most concern to artists.

- 38 % of the respondents report to have stopped their artistic activity altogether.

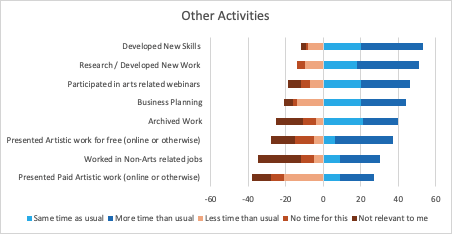

- During the pandemic, respondents report that they have dedicated more time than usual towards research, developed new work and new skills.

- The Covid Wage supplement has once again featured as the main support measure for artists.

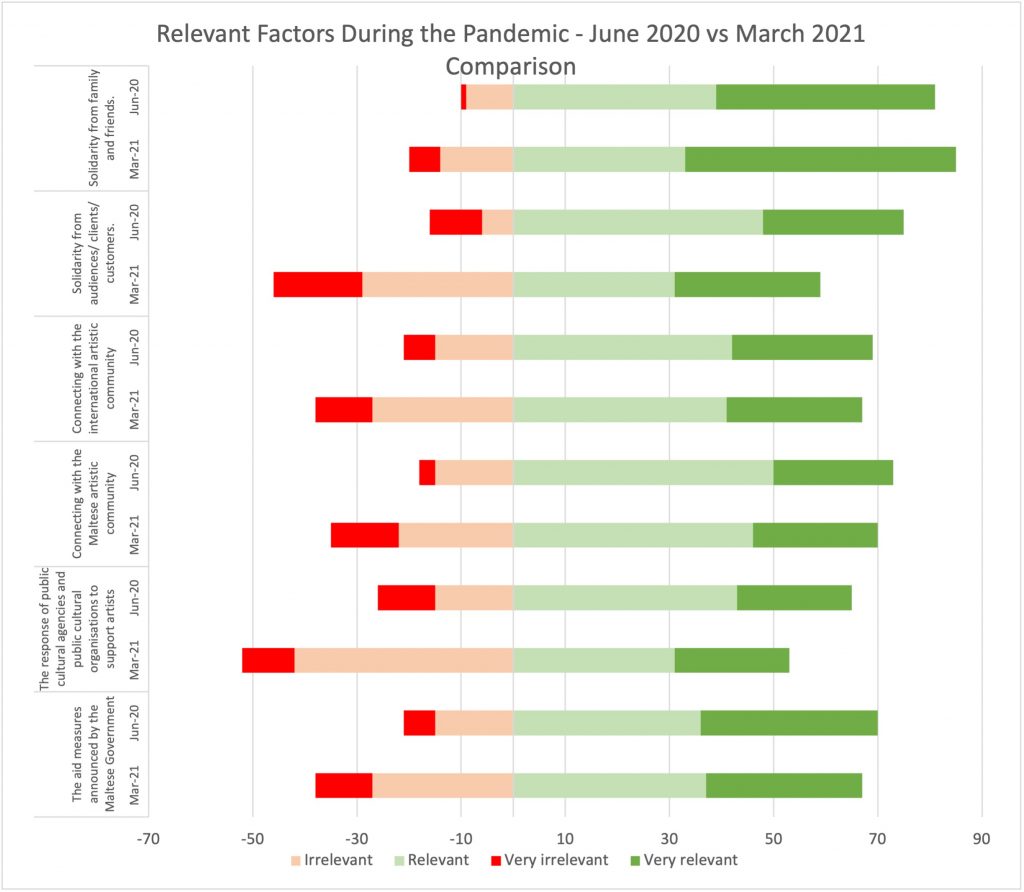

- The majority of respondents still consider solidarity from family and friends as the most relevant factor during the pandemic and the response of Public Cultural Organisations to support artists the least.

- The connection with the Maltese artistic community registered the highest increase in relevance during the pandemic. From 55% in June 2020 to 67% in March 2021.

- Most respondents agree that a post-covid plan would instil their confidence to work in the sector.

This survey is a follow up on two other surveys held in March 2020 and June 2020 as part of Culture Venture’s commitment to support advocacy for artists during the pandemic. The three surveys recorded a total of 636 responses. The latest survey was distributed among past participants of similar surveys carried out by Culture Venture in March and June 2020 and on social media and arts-related networks. A total of 110 responses were recorded out of which 5 respondents did not earn an income from the arts and therefore were excluded from the survey analysis. The survey was designed to gauge the effect of the pandemic over time on the livelihood of artists.

52.7% of the respondents declared that in March 2020, they were earning an income exclusively from the arts. The percentage of those currently earning an income exclusively from the arts drops to 48.2%. Similarly, 35.5% of the respondents declared that in March 2020 they earned a partial income from the arts but in March 2021 the percentage drops to 27.3%.

I’ve tried to keep up with training however motivation is low as there’s nothing in sight. I had to search for alternative jobs.

Circus Artist, survey participant

Labour mobility is a common trend in sectors which are saturated or under duress. The survey responses suggest that people working in the sector are occupationally mobile and are leaving the sector to seek alternative jobs and opportunities. This is further highlighted in our survey by an increase in those who are unemployed in the arts, but engaged in other sectors with a staggering increase from 2.7% to 14.5%. Whereas this is a very common occurrence as workers try to ameliorate their financial status, a sectorial brain drain from the artistic sector may have commenced.

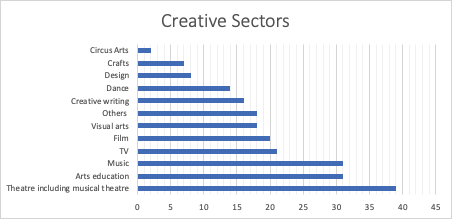

The sector distribution of respondents was as follows:

In the survey each respondent could choose more than one profession or sector, as it is common practise amongst artists to work across industries. This is a characteristic which ensures survival in normal times and promotes adaptability among artists. Something, which could significantly attribute to the tendency of artists to be occupationally mobile and change sector if they feel that their livelihoods are threatened.

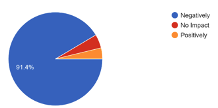

The survey shows that the vast majority of respondents (91.4%) claimed that the Covid-19 pandemic has had a negative impact on their work. Around 4.8% reported that the pandemic had no impact whilst 3.8% report that they experienced a positive effect. The results obtained are in line with data from the March 2020 and June 2020 surveys.

In spite of the roll-out of several support measures and state-aid, one year into the pandemic, respondents still feel that their industry is in status quo as per March 2020. A sectorial analysis shows that the negative sentiment comes from all artistic sectors with different impact levels defined by the type of activity.

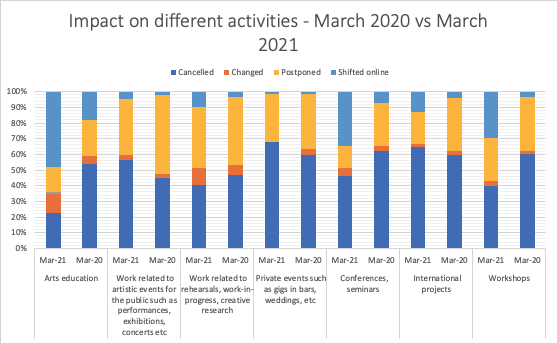

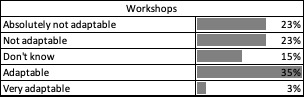

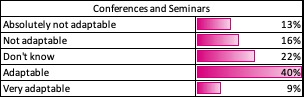

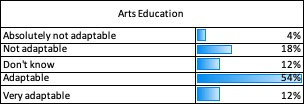

Chart 3 draws comparison between the impact of the Covid-19 restrictive measures on different activities held in March 2020 and March 2021. For Arts Education one can note that the number of postponed or cancelled activities have decreased and gave way to more online activity. A similar trend can be noted for conferences, seminars and workshops. Performances, concerts and private events such as gigs, in bars and weddings still register more cancellations and postponements.

No weddings, no international conference groups, no language student groups, entertainment venues closed, all the investment I made in equipment for rental is at a stand still. The situation is a disaster for people like me that work in the entertainment industry as a professional.

Events organiser, survey participants

The chart does not capture the absolute number of activities but uses percentages for comparative figures. However, one has to note that the number of events for the March 2021 period is significantly lower. In March 2020 respondents indicated that there were around 1,330 activities which were impacted. In March 2021 that figure goes down to 432. To put everything into perspective the number of activities is divided by the number of respondents for each respective survey. In March 2020 the ratio is slightly below 8 (7.96) activities per respondent. In March 2021 the ratio is of just below 4 (3.92) activities per respondent.

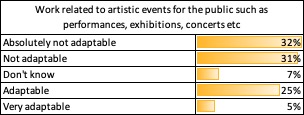

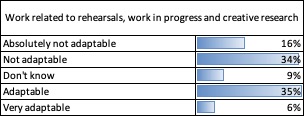

There is also a significant and understandable relationship between the level of perceived adaptability of each activity in relation to the impact. The sectors which score low on adaptability, such as international projects, artistic events and private events are those with the highest percentage of cancellations. This is quite understandable because of the very nature of these sectors. With ongoing travel restrictions international travel and networking have been very hard to commit to. On the other hand the organisation of seminars and conferences and the delivery of arts education have registered high levels of adaptability and are positively correlated with the ability to move the activity online.

The pandemic has shown that people adapt very quickly to new scenarios. With more frustration and perhaps some disillusionment, but people adapt. I was able to cope – mentally, artistically, and financially – because I happen to do operate in more than one area. If I couldn’t perform for a long while, at least I was able to write or teach (albeit online)

Performing artist, survey participant

Live artistic events and gigs are probably the worst hit areas as cancellations topped postponements. Whilst a postponement might transpire to deferred income, a cancellation more often than not, means lost income.

Young children are less likely to participate in online classes, proving difficulty for newer less established schools. Space and access is a difficulty at home & also after students have spent a day in online teaching they last thing they want is to have an online dance class – so much screen time is unhealthy.

Dance educator, survey participant

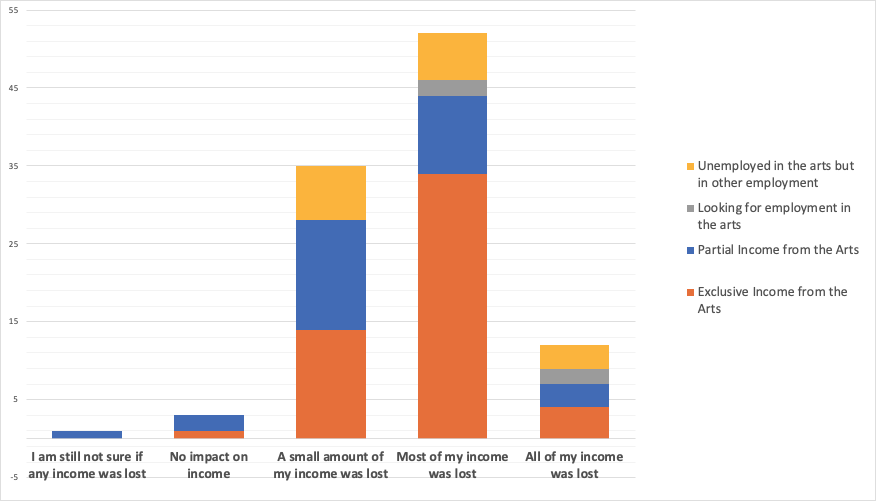

Our research continues to highlight the impact of the pandemic on income. The majority of respondents claim that during the past year (since March 2020) most of their income was lost. The highest proportion is from respondents who earned an income exclusively from the arts.

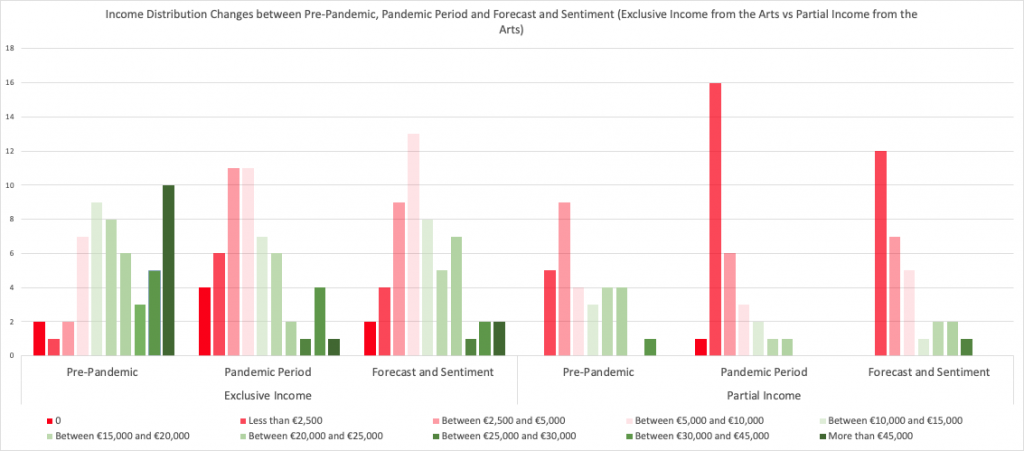

The study took a step further and tried to assess data on income across a period of time. The survey took a three-year horizon and asked participants the levels of income they registered in the pre and pandemic periods and a forecast of future income.

- March 2019 – March 2020 (pre-pandemic period)

- March 2020 – March 2021 (pandemic period)

- March 2021 – March 2022 (forecast and sentiment)

Chart 12 makes a distinction between those earning an income exclusively from the arts and those that earn a partial income from the arts as part-timers. For exclusive income earners, the pre-pandemic levels show a more or less even distribution of income across the different brackets with most respondents claiming to have received income above EUR 45,000. As the pandemic period progressed, a shift towards the lower end of the income scale is registered. The highest bracket (EUR 45K +) diminished whilst the brackets EUR 2.5K to EUR 5K and EUR 5K and EUR 10K registered significant increases. Looking ahead till March 2022, the exclusive income earners do not see much of an improvement especially at the highest levels of income. Most of the exclusive income earners forecast that they will earn between EUR 5K and EUR 10K from March 2021 to March 2022. These observations indicate that a return to a pre-pandemic level of economic activity for those earning an income exclusively from the arts, is expected to recover at a very slow pace in the immediate future.

I am now unemployed with no success of getting a job in any other sector since the job market in Malta right now, especially for younger people such as myself is not good. When I asked for the process on applying for unemployment benefits, they told me that they have such a high number of applicants that “the chances of getting the benefits any time soon is pretty much non-existent”.

Actor, survey participant

During the pre-pandemic period, most respondents earning partial income from the arts earned a total income on the lower end of the spectrum. This is to be expected since this group dedicates less time working in the arts sector, earning less than the group with an exclusive income from the arts and subsequently does not depend exclusively from the arts for its livelihood. However, this sector registered an even larger impact with almost all respondents claiming that during the pandemic period their income was less then EUR 2.5K. The income forecast for the forthcoming period amongst partial income earners remains more or less the same. These observations also shed light on the potential ripple effect on the economy. A decrease in income levels directly impacts the purchasing power of those earning that income and their dependents. This survey reveals that 56% of the respondents do not have dependants whilst 44% report that they do.

I lost my job and had to take a more menial one just to have an income but this was extremely stressful especially given that I have a family to raise.

Events planner, survey participant

Generating income has been an ongoing main concern amongst artists since March 2020 and also reflected in previous surveys carried out by Culture Venture. In this survey, generating income, the prospects of future work and personal wellbeing were once again of most concern to artists.

The main issue I had was mental health, I have never struggled with this before covid and I don’t think I’ll ever be the same again. However I have been producing some interesting work during this struggle. I expect that most other artists and creatives on the island will be severely impacted by poor mental health, so perhaps this could be a focus area for recovery in the arts sector?

Games artist, survey participant

If work is provided, honouring contracts registers the least concern as it did in previous research. However, the ability to create new work remains a concern to artists.

After 18 years of solid constant development in the industry both locally and abroad I was forced to give up my company and sell both the good name, equipment, extensive wardrobe and my venue leases to a third party.

Producer, survey participant

38 % of the respondents report to have stopped their artistic activity altogether. The remaining claim to have either continued with their regular practice (28%) or took up additional activities along with their main practice (34%).

During the pandemic respondents report that they have dedicated more time than usual towards research, developing new work and developing new skills. Artist are spending more time presenting more work (online or otherwise) which is free of charge as opposed to dedicating time for paid work.

Even though most of my art practice has ‘paused’, I have still managed to find support and motivation in learning new skills and be creative, and get two commissions.

Artist, survey participant

The level of activity and the popularity of each activity during the pandemic is more or less in line with the two previous studies conducted in March and June 2020. An emerging trend however is that the number of those pausing their artistic practice is increasing.

I have created collaborations with non essential businesses (even hairdressers) to help them out, and strengthened the online presence. Approaching Easter with restrictions on non essential business, I have turned to the physical sale of homemade traditional Easter sweets made by other youths in aid of animal welfare.

Visual artist, survey participant.

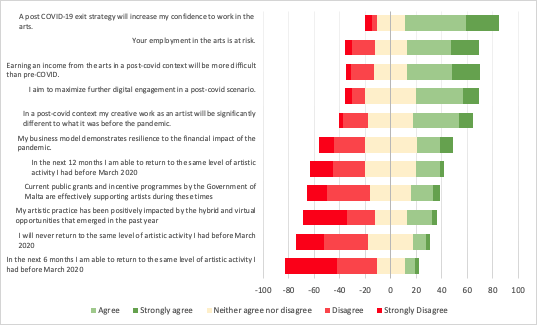

The survey also reveals the perceptions of respondents on a number of statements. Artists are not confident at all that they will return to the same level of artistic activity in 6 months’ time. The sentiment improves slightly and is perhaps is a bit more balanced on a 12-month horizon. The majority strongly disagree or disagree that they will never return back to the levels of activity held pre-March 2020. This suggests that artists are positive that the arts will bounce back, yet unclear on when or how long this will take.

This uncertainty could definitely be mitigated with a post-covid plan as most respondents agree that it would instil their confidence to work in the sector. The majority also agree or strongly agree that employment in the arts is at risk. They also believe that earning an income from the arts post-pandemic, will be harder. There might be a correlation between this and the fact that most respondents believe that their current business model is not resilient enough. Most respondents also disagree or strongly disagree that the current public grants and incentive programmes by the Government of Malta are effectively supporting artists during the pandemic.

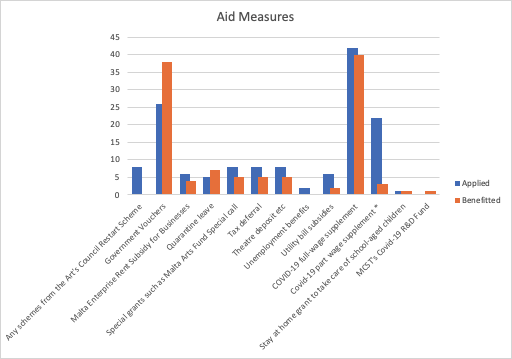

The Covid Wage supplement has once again featured as the main support measure for artists with most respondents having applied and successfully benefited from. Like all residents of Malta, the government vouchers were also a measure respondents benefitted from however is very likely that this was not an incentive by which artists could ensure more income because the activity against which such vouchers could have been redeemed was very limited. Vouchers were beneficial as a cash injection for artists as consumers and spent in other sectors. One has to note that schemes like Restart which is directly aimed towards the artistic sector, registered nil beneficiaries amongst respondents. This could also be due to the fact that the first results were announced during the research period. In fact, across the three surveys, responses to measures specific to the arts, with the first main roll-out a year after the pandemic struck, were relatively low. The low number of beneficiaries of the part-wage supplement could be due to results not being announced prior to the research being conducted.

In comparison to the June 2020 survey, respondents projected similar levels of relevance to specific factors during the pandemic. The majority of respondents still consider solidarity from family and friends as the most relevant factor. The areas which registered lower relevance were solidarity from audiences and customers and the response of Public Cultural Organisations to support artists, whereby half of the respondents claimed that they were irrelevant or very irrelevant to them. The responses on relevance of PCOs also decreased by 10% when compared to the June 2020 survey cohort. The relevance of aid measures registered a 9% decrease in relevance in comparison to the responses of the June 2020 survey. The most significant increase in relevance from both cohorts was the connection with the Maltese artistic community. This registered a relevance of 55% in June 2020 and up to 67% in March 2021. This clearly indicates the relevance of the artistic community to support artists during these challenging times.

I believe that we will come back stronger, more united through dance, willing to share our vulnerability and continue to grow through the experiences life has thrown at us, this will make us more creative, more imaginative, more connected as human beings, dancers will move in and out of the digital world but the live element of performance experiences can never be replaced or taken away, this is what we live for and this is what we have missed. We move forward together, more positively continuing our legacy. This crisis has awakened local artists to strive to be at their best.

Dancer, survey participant

This research is a Culture Venture initiative to support increased advocacy for the arts and the artists in Malta during the pandemic.